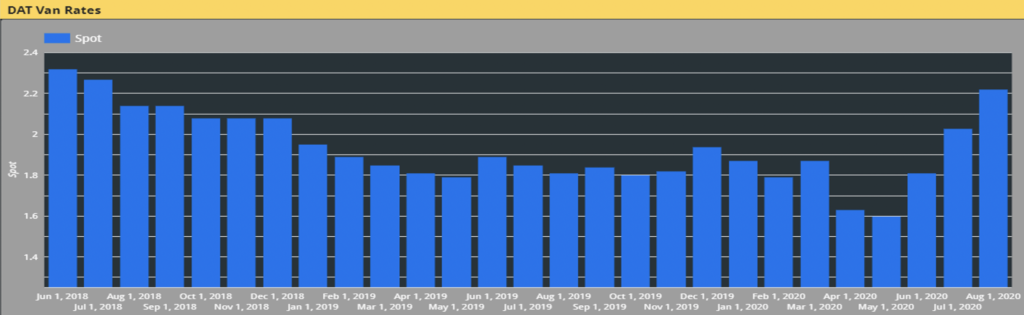

Truckload rates, especially in the spot market, continue to rise. According to DAT, the average van spot rate now exceeds contract rates for the first time since the spring of 2018. Spot rates are up over 10% year over year and 39% in the last 3 months. The increase is somewhat difficult to understand, given the continued shutdown/slowdown of a good portion of the economy.

My sense is that the surge in spot is not driven by network wide increases in volume nor significant capacity reductions, but instead, are because of carrier balance issues as certain segments of the economy are reacting in non-forecasted ways.

I would be interested in getting other’s perspectives on why spot rates are so high, as my supposition is based on feeling and not data.

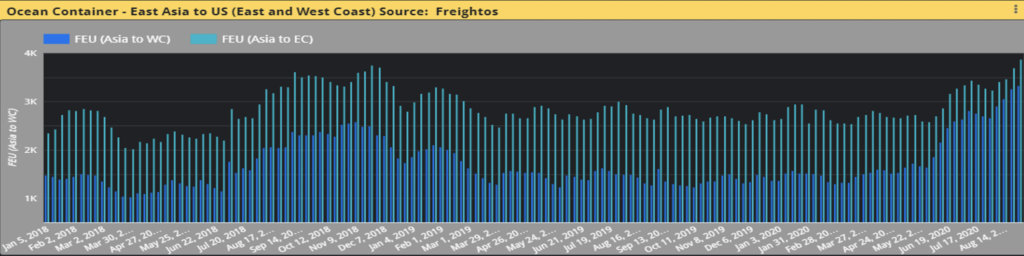

Ocean container spot rates are also extraordinarily high. According to Freightos, the average Asia to the US west coast trade lane spot rate for a FEU is up 152% since their low in mid-March and now sits at approximately $3300. The surge in spot rates is because of the steamship lines dramatically reducing capacity.

However, the largest importers into the US are Walmart, Target, Home Depot and Lowes. These companies are actually doing pretty well so the capacity did not dry up to the extent that was anticipated. One would expect ocean rates to drop in the coming months as more capacity comes back on line.

An additional point of interest is for those shippers that use west coast ports for shipments ultimately destined to the east coast, it may be time to look at east coast ports of call.

In 2018 and 2019, the average difference in spot rates between west coast and east coast ports was $1200. Today, that difference has shrunk to just over $500.

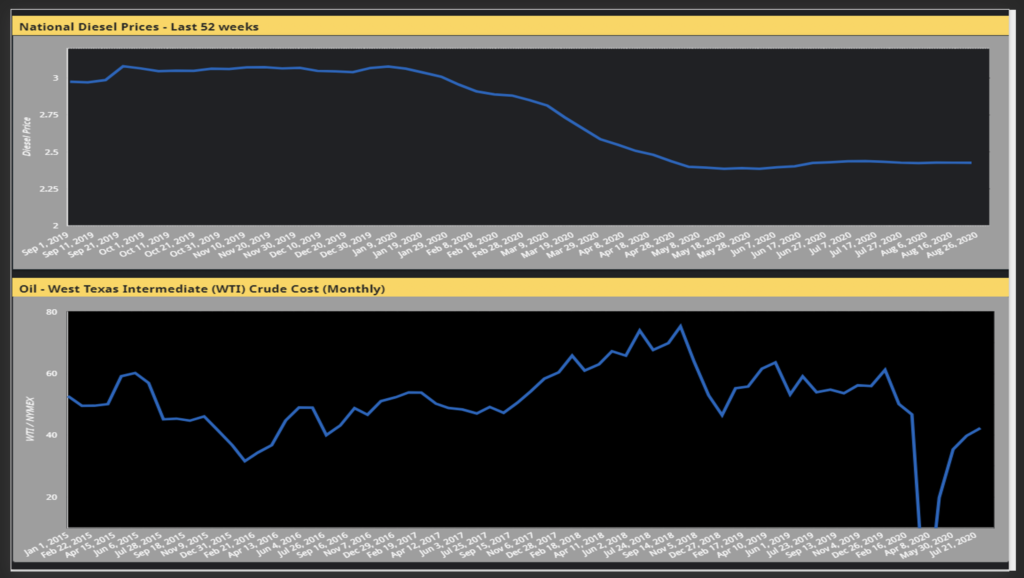

While ocean and TL rates are posing challenges, both oil and diesel prices remain in a narrow band. West Texas Intermediate seems to have found a home in the low $40s. Similarly, diesel prices are also very stable at around $2.42, rarely moving more than a portion of a penny per week.

Mike Mulqueen is a Partner at JBF Consulting and leads the Logistics Technology Strategy practice. JBF Consulting is a unique supply chain execution consultancy of TMS experts. Sign up here to receive the JBF Freight Transportation Bulletin, published monthly: http://bit.ly/JBFbulletin2020.

Founded in 2003, JBF Consulting is a supply chain execution strategy and systems integrator to logistics-intensive companies of every size and any industry. Our background and deep experience in the field of packaged logistics technology implementation positions us as industry leaders whose craftsmanship exceeds our client expectations. We expedite the transformation of supply chains through logistics & technology strategy, packaged & bespoke software implementation, and analytics & optimization. For more information, visit us at www.jbf-consulting.com