Not all milestones are good ones.

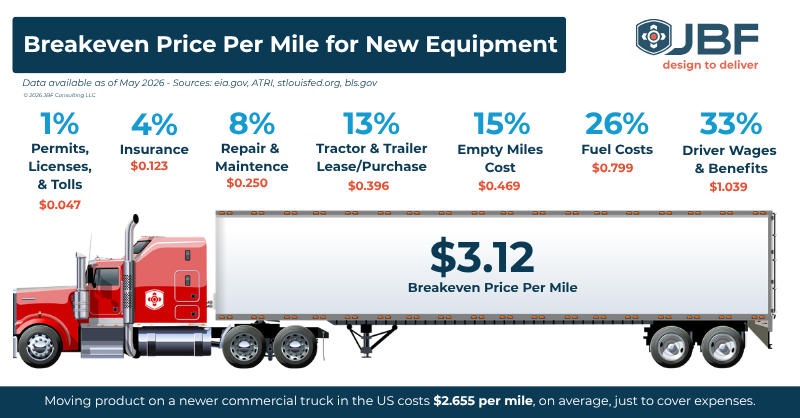

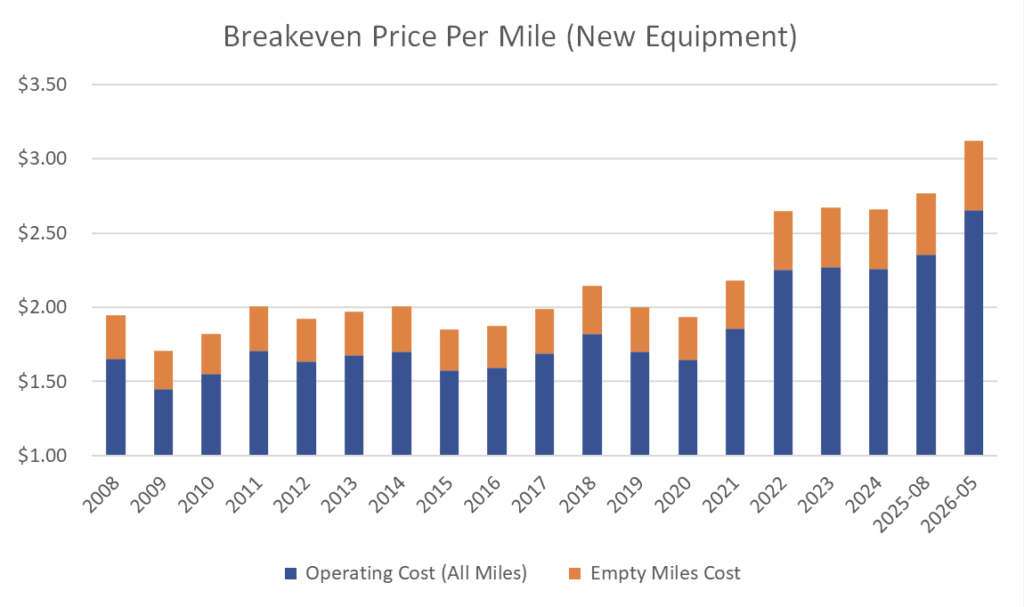

This year, the breakeven price per mile for truckload new equipment leapt past the $3.00 milestone for the first time ever and has settled at just above $3.10.

In October 2025, we predicted that prices were on a precipice and would move significantly upwards once one or more of the following occurred:

- Demand increases

- Supply-side attrition reaches a tipping point

- A large wave of older equipment must be replaced

In early 2026, we saw the beginning of all three of those market pressures start to drive prices upwards, but they were not the biggest factor that influenced rates more recently. Instead, we witnessed a steep and sustained increase in diesel cost become both the figurative and real fuel being poured onto the truckload pricing fire.

To make matters worse, that “fire” was already growing. Inflation continues to be a thorn in the side of shippers, with a 6-month Driver wage increase of 2.2% (4.4% annualized), plus continued rising new equipment costs and stubbornly high insurance rates. Carrier capacity has shrunk, and tender rejection rates have been climbing, both elements granting Carriers renewed pricing power.

What does that mean for the future of transportation prices?

Independent of fuel costs, we are in a situation where inflationary pressures will likely continue to drive truckload prices upward. Carriers and Owner Operators are simply not able to absorb even moderate increases in repair costs and insurance, and thus the industry will have to raise rates to cover them. This will be especially impactful as an increasing amount of older equipment is sunset in favor of newer tractors and trailers.

The vast majority of upcoming procurement events will see significant price increases, so plan budgets and timing accordingly. For the lucky Shippers who locked in capacity by late-2025, fuel surcharges will likely still be a major hit to the budget, but those Shippers should be in a better position to avoid near-term increases in core rates outside of fuel.

As we stand in the middle of Q2 2026, the landscape has been fundamentally reshaped by rising fuel prices. Diesel costs alone have added $0.30 per mile on average to operating costs, which translates to a price increase of $0.35 per mile from the Shipper’s perspective, where recovery for empty miles is included in the pricing (adding up to an additional 15%). A quick look at the latest DAT Dry Van Rates shows both Spot and Contract Rates jumping by approximately that amount from February to May.

Of course, there are some "golden lanes" where Carriers can link up round-trips perfectly, but those are indeed rare. There are also a few Private Fleets with substantial reverse logistics requirements that can operate close to 100% full most of the time, but for many operations, even reaching 15% empty miles is an achievement! This puts the industry in a position where not much can be done to immediately offset the recent increases.

Carriers can work to improve their load matching and attempt to limit non-revenue deadhead moves, though the imbalance in demand based on origin-destination ultimately caps any market-wide reduction.

Shippers mainly must absorb the rising fuel costs for now. They could reduce the impact by shifting to intermodal or, if they operate a Private Fleet, delaying new equipment purchases, though that introduces longer-term risk as production and materials costs are also facing upward pricing pressure. Both groups can potentially mitigate price and cost increases with better tactical optimization in the short-term and improved strategic decision-making to help keep longer-term costs in check.

Historical data based on ATRI Operational Cost of Trucking report and JBF analysis using data through May 2026.

With that, we will dig into the details around the updated 2026-Q2 numbers, with a focus on the diesel price increases and the long-term implications of today’s elevated costs. For regular readers, the below section will sound simultaneously familiar and yet very different at times from our last few posts.

Truckload Breakeven Price Per Mile is now at $3.12—an increase of $0.36 (13%) since August of 2025.

- Our updated Total Costs Per Mile estimate when using new equipment is $2.66. The additional $0.47 per mile for the Breakeven Price covers the costs incurred when a Carrier is running empty miles, generating costs that need to be recovered via increased per mile rates.

- The pricing increase associated with 15% empty miles is used to reflect the overall miles driven by Carriers, not just paid miles. Specifically, this value captures the pricing effect associated with running empty miles that are non-revenue-generating. We have applied a single percentage based on typical fleet averages, though the difficulty in finding matching loads can vary heavily depending on several factors, including geography, Shipper relationships, closed loop & roundtrip arrangements, and more.

- Fuel consumption was updated to 7.0 miles-per-gallon in our last post, to more accurately reflect current averages, which have improved as newer, more efficient equipment replaces older power units. Of course, this improvement has only partially offset the large increase in diesel fuel prices, which now account for $0.80 of the cost of each mile driven.

- Driver wages and insurance costs continue to move upwards, with additional increases in premiums likely incoming due to the recent Supreme Court decision in the Montgomery v. Caribe Transport II case. This primarily impacts Brokers, but insurance costs rarely stay isolated to only one portion of the transportation world. As before, we will be keeping a close eye on how the commercial vehicle insurance industry continues to change.

- An example of the impact on a long coast-to-cost route – say from New York City's Red Ball Garage to the Portofino Hotel in Redondo Beach, California, which covers 2,813 miles – has increased by 13% or $852, not including any empty deadhead miles to find the next load.

New vehicle costs are still 13% of the Breakeven Price per Mile when using newer equipment (15% of straight costs), but continue to rise amid tariff uncertainty and renewed equipment demand.

- Tariffs on steel, aluminum, and copper, combined with domestic labor constraints, high costs, and infrastructure limits, have led to higher prices of new equipment. Additional tariffs on imported tractors will put even more upward pressure on prices, as domestic manufacturers are unlikely to expand production capabilities until demand for new vehicles rises significantly from current levels.

- In October, we noted that the rising cost of new equipment would likely increase demand for used vehicles, which indeed happened. This then caused a ripple effect, where new vehicle orders rebounded, as used equipment prices began to rise. This has resulted in price pressure on both new and used equipment, further exacerbated by pent-up demand, as fleets could only delay replacing aging equipment for so long.

- If fuel prices stay elevated for much longer, prices will further increase due to the inflated cost of transportation involved in manufacturing and delivery of finished equipment. It often takes months to get new vehicles delivered once ordered, meaning that fuel price uncertainty could linger much longer after prices eventually subside. Commercial equipment manufacturers will have to employ ways to mitigate that risk, either through adjustable pricing based on fuel costs at time of production or by simply increasing prices.

Per mile Spot Rates have spiked from just over $2.00 in August 2025 to over $2.80 in May 2026.

- We noted in our 2024 update that a realistic absolute floor for the Spot market was $1.85 per mile. To put that in perspective, for new equipment and applying average national Driver wages but with zero fuel, total cost is now $1.85 per mile. Even with Owner Operators sacrificing wages & benefits and holding equipment as long as possible (7.3 years / approximately 588,000 miles for power units according to the ATRI 2024 respondents), it is unlikely that we see Spot Rates drop below $2.40 per mile any time soon. There could be a major economic event that sees prices slip below that, but Carrier attrition would not let it last long.

- Overall, fuel costs have put even more pressure on margins, but this great market reset creates an opportunity to permanently raise base rates. Many Drivers/Carriers operated with minimal profit, or even at a loss, for multiple years, which was not a viable long-term operating model. We are now seeing the start of a new pricing era, where Carriers have greater leverage and can begin to recoup their prior losses.

What is the net result of the recent increase in diesel prices amid continued inflationary pressures?

Rising fuel prices will ultimately establish a new price floor. Eventually, something was going to push up prices, be it operating costs, demand, supply – or a combination of all three. Even before diesel began increasing in March, truckload spot and contract rates had begun to converge at $2.40-$2.50 per mile due primarily to Carrier attrition after a lengthy, multi-year period where Shippers had the upper hand.

We anticipated in October of 2025 that a convergence in the Spot and Contract prices would likely be the first sign of a broader market correction. Unfortunately, that timing happened to coincide with spiking diesel prices, making it very difficult to lock in decent rates unless Shippers already had a solid working relationship with their Contract Carriers. Overall, the opportunity for Shippers to negotiate favorable Contract rates has expired, especially with so much economic and political uncertainty added to the mix.

There are far too many unknowns around how long fuel prices will remain elevated, but once the dust settles, it is highly unlikely that truckload prices will return to the average $2.00 per mile Spot rates, nor the $2.40 Contract rates that were prevalent a year ago. Given the amount of aging equipment, increasing Driver costs, and lower Carrier capacity, the new nationwide average is likely to settle around $2.50 per mile for Spot rates and slightly higher for Contract rates.

As with any pricing prediction, events such as a major recession or, conversely, significant renewed investment in the industrial sector could tip national average truckload prices either side of that number. And there is a growing possibility that diesel prices stay elevated for several more months, which in turn puts transportation-related inflationary pressure on manufacturing new equipment. That would be the start of another price-hike cycle, as old equipment is replaced with significantly more expensive newer items.

What, if anything, can be done to mitigate rising prices and operating costs?

We previously advised Shippers with existing Private Fleets to evaluate increasing the size of their fleet, but now that both used and new equipment prices have increased, the potential savings are somewhat limited for most Shippers. It is difficult to know the next time an equipment purchasing opportunity will arrive, but for the foreseeable future, lease/purchase prices will remain elevated.

One savings element for Shippers with access to a Private and/or Dedicated Fleet has not changed: leveraging those resources to service specific lanes. The key is to identify the higher-priced Carrier lanes and assign Private Fleet assets to service them, while using a combination of Contract and Spot Rates where the market still supports lower-priced lanes.

Regardless of your current situation, improvements in technology, people, and processes can help set the foundation for policy and operational changes to offset significantly increased prices. With rising truckload prices upon us and more uncertainty than ever, Shippers will need robust planning—combined with a well-designed Transportation Management System (TMS) solution—to take advantage of the constantly shifting landscape. Many annual planning cycles will start in the coming months, so consider requesting budget for improving or selecting a TMS that fits your specific needs, whether that entails improved mode selection, leveraging zone skipping, adapting to changes in Spot Rates, or maximizing your Private Fleet utilization.

Each company has its unique combination of challenges and opportunities. If your company could use extra support in identifying where to spend your precious time and money, reach out to a trusted partner and have them take an objective look at your current situation. Afresh view of your people, technology, processes, data, and policies will prepare your business to embrace the new level of transportation costs, where each mile saved and efficiency uncovered is more important than ever.

About the Author

Chris Doersen is a Principal of Client Engagement at JBF Consulting, bringing more than 20 years of experience designing, modeling, and implementing logistics solutions for complex transportation networks. He partners with global shippers to drive efficiency, optimize fleet and carrier operations, and enable technology adoption that delivers measurable impact. Chris has deep expertise with platforms including Blue Yonder, Descartes, Llamasoft, and Appian, and has led large-scale network design and TMS implementations for leading manufacturers and distributors. Known for his analytical rigor and operational insight, Chris helps organizations turn transportation strategy into sustained results.

FAQs

As of Q2 2026, the truckload breakeven price per mile has reached $3.12 — a 13% increase ($0.36) since August 2025. This marks the first time in history the breakeven price has surpassed the $3.00 milestone.

Several factors are driving truckload rate increases in 2026: a steep rise in diesel costs (adding approximately $0.30 per mile to operating costs), driver wage increases of 4.4% annualized, rising new equipment costs due to tariffs on steel and aluminum, higher insurance premiums, and shrinking carrier capacity with rising tender rejection rates.

Dry van spot rates have climbed from just over $2.00 per mile in August 2025 to over $2.80 per mile in May 2026. Analysts expect the new floor for spot rates to settle around $2.50 per mile even after fuel prices decline, due to sustained carrier attrition and rising operating costs.

What can shippers do to reduce the impact of rising truckload prices? Shippers have several options to mitigate rising truckload costs: shifting freight to intermodal where feasible, leveraging private or dedicated fleet assets on higher-cost lanes, using contract carriers rather than relying on volatile spot rates, and investing in a Transportation Management System (TMS) to improve mode selection, load optimization, and strategic lane planning.

Shippers have several options to mitigate rising truckload costs: shifting freight to intermodal where feasible, leveraging private or dedicated fleet assets on higher-cost lanes, using contract carriers rather than relying on volatile spot rates, and investing in a Transportation Management System (TMS) to improve mode selection, load optimization, and strategic lane planning.